Dr Hans Sievertsen and Professor Sarah Smith explore economists’ views on different issues, including the current COVID crisis, and ask whether there is such a thing as a one-handed economist.

Dr Hans Sievertsen and Professor Sarah Smith explore economists’ views on different issues, including the current COVID crisis, and ask whether there is such a thing as a one-handed economist.

“Give me a one-handed economist”, demanded Harry Truman, the former US President. “All my economists tell me, on the one hand… but on the other …” Economists get a lot of stick when it comes offering diverging views. In a similar vein, George Bernard Shaw joked that if you laid all the economists in the world end to end, you wouldn’t reach a conclusion. Why do people love to mock economists’ ability to give a clear answer? Is it really the case economists can’t agree on anything?

The expert view

For nearly a decade, The Initiative on Global Markets (IGM) Forum at Chicago Booth Business School, has been asking leading economists for their views on topical economic issues. The expert panel consists of around 50 academic economists in the US and 50 academic economists in Europe who are at top institutions, including Harvard, Stanford, MIT, Berkeley, Yale, LSE, Oxford, UCL, Sciences Po, Trinity College Dublin, Bocconi, Stockholm. Each week, they are asked for their views on everything from climate change to BREXIT to the state of the economy to individual economic policies, such as the minimum wage. Their responses, across a nearly 400 questions that have been asked, provide a unique insight into how economists think about different issues.

The first thing to emerge from looking at the responses is that there is a high level of agreement among economists. Yes, that’s right – economists (broadly) agree! Very few economists vote against the consensus view on any topic – out of 100 economists that answer a question, only eight or so will express an opinion that is opposed to the majority view. On nearly one-third of the questions, there are no dissenting voices at all. Some of the issues on which economists are unanimous are that free trade generates net benefits to society, that imposing income taxes will cause a change in the tax base (by changing people’s actual behaviour or reporting patterns), that investors cannot out-perform the stock market on a persistent basis, that making drugs illegal increases their price and that not getting vaccinated against contagious diseases imposes costs on other people.

However, even expert economists are often reluctant to give a definite opinion. On each issue, the possible responses they can give are either (strongly) agree or (strongly) disagree, or to say they are uncertain. The “uncertain” response is chosen in nearly one-third of cases and by the majority of respondents on a range of issues including whether a tax on digital activities is a good idea, whether chief executives are paid too much, whether income tax cuts would increase GDP and whether local governments should curb gentrification. The one-handed economist problem is not so much that economists have evenly divided views on the same topic but that individual economists are often reluctant to give a firm view.

Why are economists uncertain?

One reason why economists are uncertain is when a question falls outside their specific area of expertise. Economics is a very broad subject covering many different “fields” and economists tend to specialise in one or two fields – international trade, development economics, the financial system, the macro-economy, labour economics, firm behaviour or government tax and spending policy. The panel members are 14 per cent more likely to give a definite answer (i.e. not answer uncertain) if the question falls within their area of expertise. If you want to find a one-handed economist, you are more likely to do so if you pick one in the right economic field to answer the question.

A second reason is that, in many cases, the questions the panel members are asked are not about economic models or economic evidence, which economists might more easily agree on, but are about whether something is “good for society”. Economic policies typically require trade-offs, imposing costs and benefits on different groups in society. Deciding whether a policy is a good idea (overall) means deciding whether the benefits to one group outweigh the costs to another. This involves making a value judgement that many economists may be reluctant to make. An economist can tell you what are some of the costs and benefits, but making the trade-off is a political judgement. Policy-making around COVID19 is no different. The government’s scientific advisors can provide the available facts and their best advice, but the science does not dictate a single course of action and ultimately the decisions, and the trade-offs, rest with the politicians.

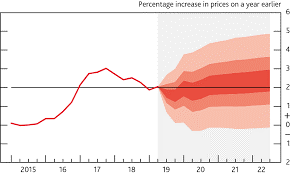

The third reason is that there is inherent uncertainty in many economic questions. Economists use economic models to understand and predict behaviour and economic data to validate – and fine-tune – their models. However, modelling something like the UK economy is hugely complex, involving the actions and interactions of millions of individual people and firms. The data that is available to measure what has happened may be imperfect, and, when it comes to predicting the future, simply not there. Ironically, economists are mocked just as much for making (over-precise) predictions about the economy as they are for their reluctance to reach a firm conclusion. “The only function of economic forecasting is to make astrology look respectable”, joked (economist) Ezra Solomon. Many self-respecting economists, recognising the inherent difficulties in looking into an economic crystal ball, are reluctant to give a precise answer. The Bank of England displays its predictions of future inflation rates using fan charts (an example is shown below) which show the range of price increases they expect – sometimes, being uncertain about exactly what the future holds is the only certain thing that economists can say.

Fan chart: Bank of England’s inflation projection

The chart shows the range of possible outcomes for future inflation rates. Based on the Bank of England’s model, the outturns of inflation are expected to lie within each shaded zone on 30 out of 100 occasions, implying a 90 per cent probability that inflation will lie (somewhere) within the fans.

Expert views on COVID-19

Currently the most pressing economic questions are about the impact of COVID19 on the economy and how to chart a way out of lockdown that will not trigger a second wave of the pandemic. The IGM Forum has asked its experts for their views on these topics. The answers show a very high degree of consensus among economists on both side of the Atlantic and a much higher degree of certainty than usual.

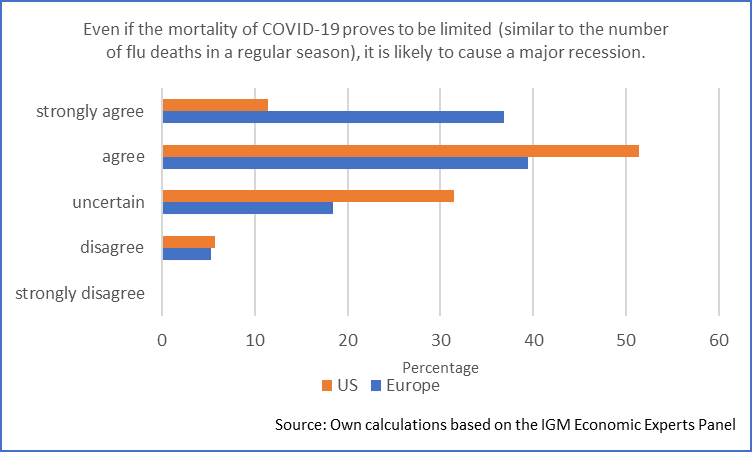

The first question asked in the second week of March (early in the pandemic) was about the likelihood of a recession. The responses are shown in the chart below. 76 per cent of the European expert economists and 63 per cent of US economists agreed that there would be recession. There were only dissenting two voices in each sample. Some were uncertain (nearly 20 per cent of the European sample and more than 30 per cent of the US sample, possibly higher in the US because the pandemic hit slightly later). But this level of uncertainty is notably lower than among the sample of all questions (one-third). Even in the early stages of the pandemic, there was a strong economic consensus, particularly in Europe, that a recession was on the cards.

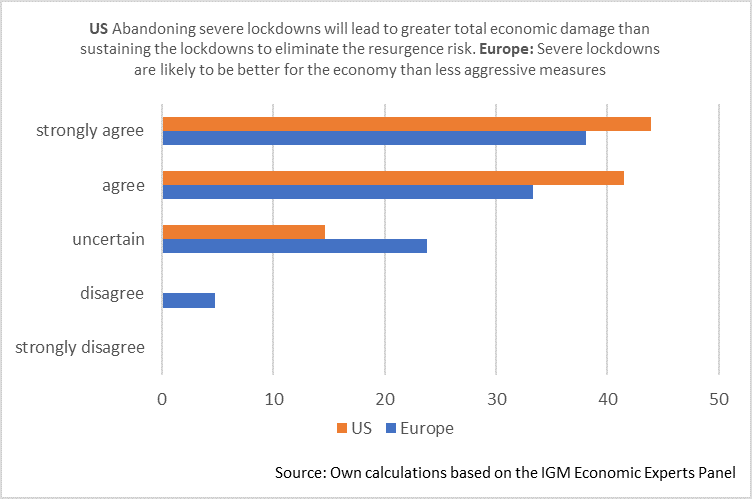

Currently, governments in Europe and the US are grappling with how to ease lockdown. This has often been presented as a “economy versus health” questions – lockdown must be eased to get the economy going again, but this threatens a second wave of the pandemic. The views of the expert panel are that there may be less of a trade-off than is sometimes suggested and that coming out of lockdown too early poses an economic risk as well as a health one. 85 per cent of US economists and 71 per cent of European economists agreed that maintaining stricter lockdown was better for the economy in the medium term than coming out too early. There were few dissenting voices – and less uncertainty than on most other questions.

Take-aways

Economists are often mocked for not giving a clear opinion. Looking at the data, there is a very high degree of consensus among economists on many topics, but also a willingness among expert economists to admit they are uncertain. Uncertainty arises both because many economic questions are inherently complex and uncertain, making it hard to give precise answers, but also because economists are often asked questions that contain inherent value judgements that lie outside their economic expertise. When it comes to COVID19, however, there are plenty of “one-handed economists” – early on there was a clear consensus (with a high level of certainty) that the pandemic would cause a recession, also that coming out of lockdown too soon would have an even greater economic cost.